FINANCIAL

RAPE - Councillors Goring and Himmler, found a way to fleece

more innocent victims, on their way to the (virtual) gas

chambers of commerce. At least property owners get a nice shower

as they are led to the cremation pits. Wealden is going up in

economic flames, as their officials aim at their Final Solution! You tell us,

what is the difference between such actions and Nazi Germany

liquidating the belongings of those exterminated in special

camps? You may think moving to Wealden was not your best

decision. We are.

BANKRUPTCY DEFINITION

When an organisation is unable to honour its financial obligations or make payment to its creditors, it files for bankruptcy. A petition is filed in the court for the same where all the outstanding debts of the company are measured and paid out if not in full from the company's assets. A Chapter 7 bankruptcy can stay on a credit report for up to 10 years from the date the bankruptcy was filed, while a Chapter 13 bankruptcy will fall off a report seven years after the filing date. After the allotted seven or 10 years, the bankruptcy will automatically fall off your credit report.

Obviously, those responsible for creating the bankruptcy, must not be allowed back into office for at least seven, but more like ten years. And if found guilty of procurement fraud, should be banned for life from any political position of trust, involving public funds. The alternative, is constant monitoring of any politician's assets and accounts, using anti money laundering computer algorithms.

Corrupt politicians should be treated as social terrorists.

And totally independent policing, not involving local constabularies, who are themselves corrupt in many cases.

Such as is demonstrable with Sussex

police refusing to investigate planning frauds within Wealden

District Council (WC). Worse still, providing blank police

headed paper to WC, for them to write their own letter of

exoneration, having failed to interview any of the informants,

to take their evidence. This case is ongoing, not investigated

from a Petition

presented in 1997. With no statute of limitations on fraud

and conspiracy to pervert the course of justice. Historic crimes

no longer fade away. Historic sex crime investigations sometimes

go back 30-40 years - in the public interest. With irresponsible

borrowing now up to £2.46 trillion pounds, the sums expended on

cover-ups, brings such lack of transparency and accountability

into stark relief. Especially, where there is still a cost to

the cover-up. In other words that fraud is still live.

HOW

WOULD BRITAIN DECLARE SOVEREIGN INSOLVENCY

In

the case of a Country declaring itself insolvent, in a

paper/printed/digital currency situation, the Peak Debt, the

threshold for debt service as a percentage of income, must not

be surpassed. If it is, then the country owes it to all

creditors to tell them it cannot honour its financial

obligations.

UNFORTUNATELY,

NOT A JOKE - Held to be the Anti-Christ

of British politics, candidates like Boris Johnson and Margaret

Thatcher, would no longer be able to treat the electorate

like disposable assets, as in British

Empire days - to keep their wealthy party supporters in the

lap of luxury. So, sustaining a class system and slavery. The

Big Red Bus 'lie' should be sufficient to change statute, to

prevent the lesser informed electorate from being deceived, and

so, in effect, voting to increase national debt and ultimately

hardship. Election campaign rules should be continuously monitored

and enforced to ensure truthfulness from candidates.

TERMINAL INSOLVENCY TRAJECTORY - ARMAGEDDON

Peak debt is a threshold for debt service as a percentage of income that, once surpassed, makes it impossible for the debtor to be able to use new debt to invest for growth that will allow for income growth in excess of debt-service growth.

That Nation enters a Red Growth

period, as opposed to Blue

Growth.

Once that threshold has been exceeded, the debtor is on a terminal insolvency trajectory. The debtor may continue to issue new debt to continue to service the old debt and to pay for other expenses as long as creditors allow, but eventually default will have to occur.

The reason debtors are allowed to continue to borrow even after they are terminally insolvent and default is inevitable is principally a reflection of asymmetrical information access. Debtors know before creditors when they have exceeded the solvency threshold.

This applies to all borrowers.

The pervasive memes in the financial sector are that currency-issuing governments cannot become insolvent simply because they "issue" their own currency, and central banks rebate interest income to their respective government treasuries.

The general meme is that because they can always "issue" new currency to pay the interest on debts denominated in their currency, they can always have the funds to pay the interest and thus can never become insolvent.

This is simply false given the way currencies enter economies, which is the same globally.

Although central banks electronically create currency at no cost, that currency has no value until it enters the economy. Currency enters an economy in swap for existing assets, normally in return for sovereign debt held by the private member banks of the central bank.

That means the currency has been loaned into the economy, not printed into the economy. If it were printed into circulation, it would enter as a "credit" rather than as a debt.

There is nothing that prevents sovereign governments from issuing currency as a credit, rather than as a debt, but that's not the way the global monetary system works now, and hasn't since every country has converted to central banks lending money into circulation over the past 100 or so years.

The ability to borrow money into existence was restricted by the

World War

II-era Bretton Woods monetary system, but that largely ended when the U.S. dollar's convertibility into

gold was terminated by President Nixon in 1971.

In order for a currency-issuing country to avoid insolvency, the currency entering the economy in swap for sovereign debt must cause economic activity, and tax receipts as a result, to be greater than the cost of servicing the sovereign debt over a long period of time.

If that occurs, the currency will maintain its value. If it does not and the currency-issuing economy exceeds the solvency threshold, which is the point at which more than 25% of tax receipts are required to service existing debt, the country becomes terminally insolvent.

Once the threshold is exceeded, no changes of any kind can reverse the terminal insolvency trajectory. Changing taxing schemes, deregulation and increases or decreases in government spending are rendered mathematically inoperative as mechanisms for creating economic growth, and thus tax receipts that exceed debt service requirements.

As

we understand it, Japan is headed down this road, with the US

not far behind. That leaves the UK next in line, as a result of

present policy inadequacy.

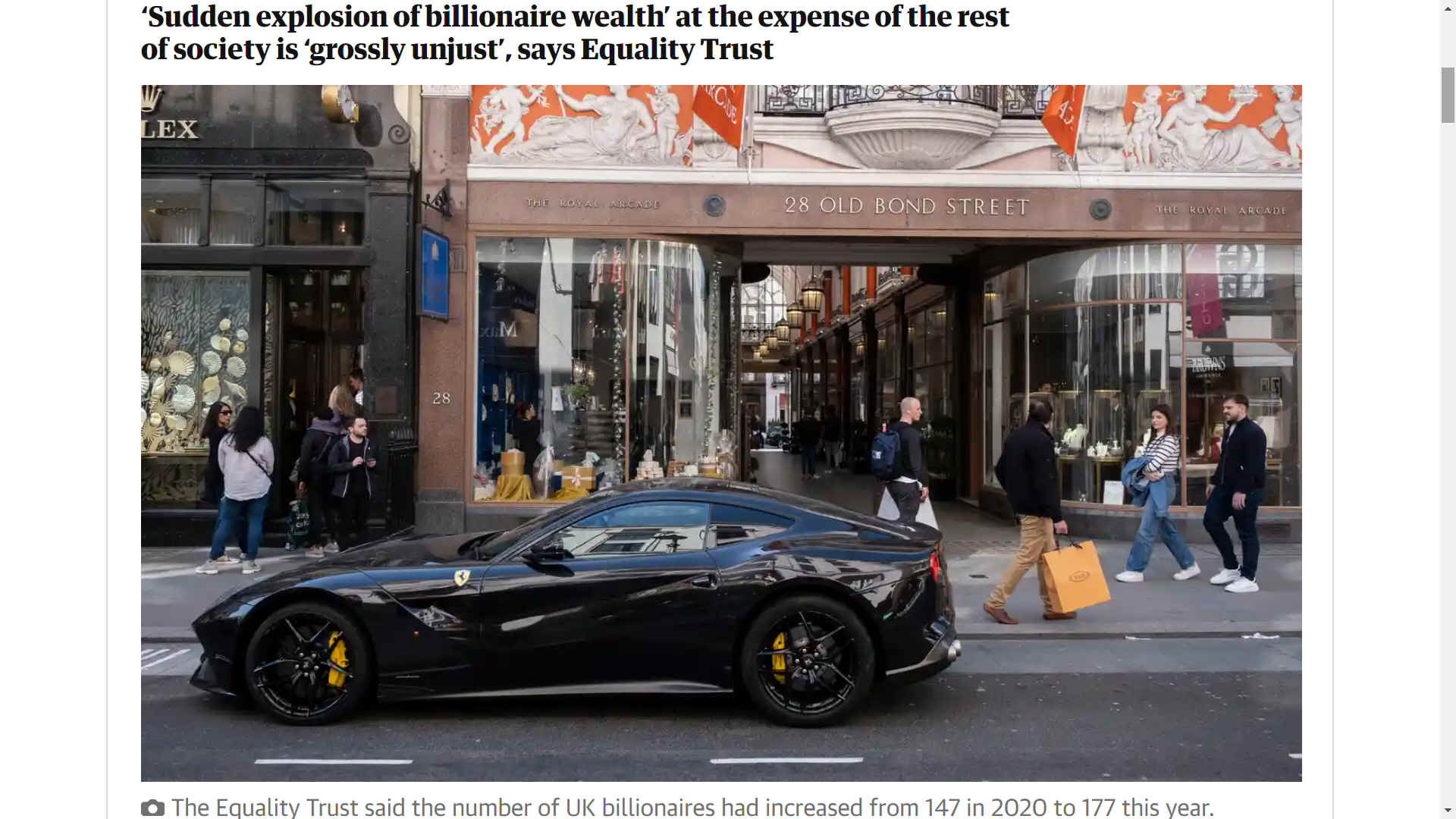

There

may be a link between the explosion of billionaire wealth, and

policies that keep on issuing currency credits. It is all false

and unsupported credit, that allows market manipulation with

relatively few checks and balances. Because, countries in

difficulty do not want checks and balances against their own

ineptitude.

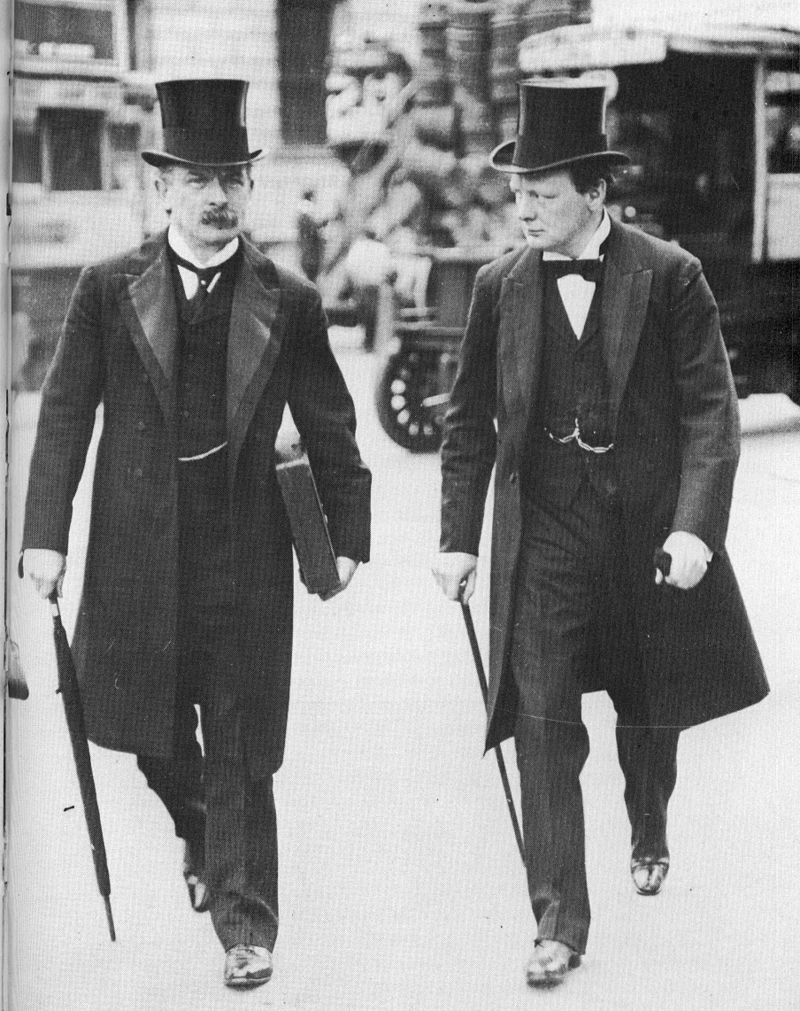

Two

of the greatest social reformers in British politics, Lloyd

George and Winston

Churchill. The Trade Descriptions Act 1968 came into effect on 30 November 1968. It replaced and expanded the old Merchandise Marks laws dealing with mis-description of goods in general and its particular job is to ensure, as far as possible, that people tell the truth about goods, prices and services.

We think this should apply to politics and politicians.

DECLARING

(OR SEEKING) A MORATORIUM - A BREATHING SPACE

A moratorium period defines a delay in an activity when an unforeseen situation arises. Such a period remains in force until the conditions return to normal times. For example, in bankruptcy law, a loan moratorium allows debtors to suspend the legal obligation of repayment of loans.

Over a moratorium period, a borrower is not required to make a payment over the period. In addition to the distinct difference as outlined above, a moratorium period length can range from weeks to months, whereas a grace period length

for small scale debt is usually 15 days.

A temporary suspension of an activity or law is effective until future consideration warrants lifting the suspension, such as if and when the issues that led to moratorium have been resolved. A moratorium may be imposed by a government, by regulators, or by a business.

Moratoriums are often imposed in response to temporary financial hardships. For example, a business that has exceeded its budget might place a moratorium on new hiring until the start of its next fiscal year. In legal proceedings, a moratorium can be imposed on an activity such as a debt collection process during bankruptcy proceedings.

As an example, in 2016, the governor of Puerto Rico issued an order to limit the withdrawal of funds from the Government Development Bank. This emergency moratorium established a hold on withdrawals that were not related to bank principal or interest payments in order to reduce risks to the bank's liquidity.

On the voluntary side, insurance companies will sometimes issue moratoriums on writing new policies for properties located in specific areas during the course of a natural disaster. Such moratoriums can help mitigate losses when the probability of filed claims is abnormally high. For example, in February 2011, MetLife issued a moratorium on writing new policies in many Texas counties due to an unusual outbreak of wildfires.

COVID 19 & LOWER INCOME ECONOMIES (LIEs)

LIEs have different alternatives to organise a debt moratorium on their external obligations. An optimal mechanism to deliver financial relief would be a multilateral framework for a comprehensive debt moratorium and relief, organised by the UN. A multilateral approach would ensure that the measures adopted are comprehensive and provide special and differentiated treatment to small and vulnerable countries.

However, in a scenario of multilateral inertia where debt relief is used as a tool for the introduction of

condition-alities and structural adjustment, countries experiencing a humanitarian emergency caused by Covid-19 could declare a sovereign unilateral debt moratorium. The human rights imperative to protect lives at risk would provide all the justification necessary for the adoption of this approach.

From a financial perspective, there are at least three complementary options, depending on the types of external debt covered by the moratorium:

1. A debt moratorium on IMF and World Bank payments: The most immediate alternative is for debtors to coordinate a moratorium on payments to the IMF and World Bank for the concepts of principal repayments, interest and charges. This procedure would require a majority vote of the Board of Directors of both organizations. Given the circumstances, the IMF and World Bank can take the initiative and accelerate the declaration of a broader moratorium covering other creditors. A moratorium for 2020 would free up to US$ 3.8 billion without any type of policy

condition-alities. An extension until 2021 would release an additional US$ 4.8 billion, for a total of US$ 8.6 billion.

2. A debt moratorium on external official creditors: A broader debt moratorium covering all official external creditors of the public sector in LIEs could free up a total of US$ 19.5 billion in 2020. An extension until 2021 would release an additional US$ 18.7 billion, for a total of US$ 38.2 billion. Countries currently assessed to be at low and moderate risks of debt distress would be the main beneficiaries. A key element to achieve an immediate moratorium is the coordination amongst bilateral creditors, mainly Paris Club members and China, in order to avoid a situation where resources freed up end up potentially being used to pay other creditors. However, even without a multilateral agreement, debtor countries in a situation of humanitarian emergency can address creditor coordination failures and promote a wider agreement on the issue by adopting a sovereign unilateral debt moratorium.

3. A debt moratorium on external private creditors: The moratorium could be expanded to cover private external creditors to the public sector. A policy designed for 2020 could release up to US$ 5.9 billion in additional resources previously tied to debt service. Extension into 2021 would add US$ 6.2 billion for a total of US$ 12.1 billion. Countries currently assessed to be at high risk of debt distress would be the main beneficiaries. A multilateral framework for a debt moratorium, coordinated under the auspices of UN, could request the US, UK and the EU for the introduction of a temporary stay on sovereign debt litigation in order to protect vulnerable countries from vulture funds aiming to profit from the crisis

After the COVID 19 crisis, countries may consider a shift to a new paradigm where debt sustainability is assessed with respect to the financing needs of Agenda 2030. Enough debt relief must be granted to allow countries to fund their national programs to achieve the SDGs. Until then, we need to remind ourselves that no-one is safe until everyone is safe.

On October 4, 2022, the LA city council voted to wind down the eviction moratorium that had been in place since March 2020, making it one of the longest COVID tenant protections in the country. Non-payment of rent cases will be allowed to resume in February 2023.

THE NITTY-GRITTY

The fallout from the economic crisis of 2008 was not limited to troubled homeowners, mortgage lenders, and major financial institutions. The crisis spread further, leaving entire nations facing financial ruin. A national insolvency is not a simple matter of a country going to court and filing for bankruptcy. Rather, a nation going bankrupt triggers serious economic consequences at home and abroad, often requiring rescue from foreign investors or global institutions such as the International Monetary Fund.

The German newspaper "Spiegel" reported on the issue of national bankruptcies in 2008, after the island nation of Iceland neared insolvency. When a country can no longer pay the interest on its debt or convince anyone to lend it money, it has reached bankruptcy. Possible causes of a country’s bankruptcy can include war or financial mismanagement by the government, the newspaper reported.

An entire nation becoming financially insolvent is not a new phenomenon. "Spiegel" reported in a 2008 article that Germany went bankrupt twice in the 20th century: once in 1923 after World War I and again after the end of World War II in 1945. Since then, the newspaper reported, Russia has gone bankrupt in 1998, followed by Argentina in 2001. In 2008 Iceland became the first country to fall victim to the financial crunch that resulted after the collapse of the U.S. housing market. "Spiegel" reported that other countries, including the Ukraine and Pakistan, face financial ruin as well.

When a nation becomes bankrupt and defaults on its loans, central banks may try to attract additional foreign investors by raising the interest rates on the country’s bonds. "Spiegel" reported that Iceland’s central bank raised its prime rate to 18 percent in 2008 while Venezuela offered 20 percent interest in hopes of selling its bonds. Such large hikes in interest rates negatively impact the credit ratings of the countries themselves, which "Spiegel" said often results in lenders writing off the loans the countries can no longer repay.

When a country reaches bankruptcy, massive inflation is the likely outcome for the country’s consumers and businesses. Stock prices often plummet, along with the value of the nation’s currency. As the value of money falls, bank runs may result as panicked citizens rush to withdraw cash from their accounts. This occurred in Argentina in 2001 after the government there froze bank accounts, limiting the amount of money people could withdraw. "Spiegel" said many desperate Argentines even slept in front of ATMs, hoping to withdraw what cash they could.

In some cases, social and political unrest can result if a nation goes bankrupt. In Argentina, angry residents rioted and looted supermarkets in the wake of the country’s 2001 insolvency. In Iceland, the head of the country’s central bank was forced to resign after that country’s crisis, which cost thousands of Icelanders their jobs and life savings, according to a 2009 report by "The Times of London."

To avert bankruptcy or to cope with its effects, insolvent governments often look abroad for a bailout. Nations in the most dire straits seek emergency loans from the International Monetary Fund (IMF). Recipients of IMF assistance have included Hungary and the Ukraine. IMF assistance, however, comes with strings attached. In exchange for IMF help, "Spiegel" reported, the Ukraine was forced to freeze social spending, privatize some government services, and increase natural gas prices.

In 2009 Harvard historian Niall Ferguson predicted that a growing number of European nations were in danger of bankruptcy. In a report by "The Guardian" newspaper of the United Kingdom, Ferguson said Ireland, Italy, and Belgium were in the greatest danger of bankruptcy, with the U.K. also at risk.

THE ADVANTAGES OF INTERNATIONAL DEBT & GDP

International debt or the ability of governments and corporations to raise money outside of their country is vital in maintaining economic and financial liquidity. The most recent example of the advantage of countries or governments raising money through International debt is that of Greece during the recent Greek debt crisis. Strapped for cash, the government’s last resort to paying interest on its external debt and also managing the day to day running of its business was borrowing money from other countries.

International debt or money owed by the government of one country to that of another can be in the form of bonds, treasury securities, as in the case of the U.S., or negative trade balance. Trade deficits mean an excessive borrowing nation is able to achieve a higher living standard and is able to provide domestic investment that in turn spurs future economic growth, facilitating repayment of debt. Fostering future economic prosperity is a positive outcome of International debt in many cases.

So when a country is facing budget deficits or there is paucity of money due to high debt to GDP ratio, a country can turn to international debt and raise much-needed money. Later as it emerges from the crisis, it can repay the interest and the principle amount in installments. In fact, money borrowed from other countries can be invested to spur the economy toward reviving GDP.

It is a risky strategy, dependent on the Nation in trouble, being able to persuade entrepreneurs to rise to the challenge.

DEVELOPING COUNTRIES AND INTERNATIONAL DEBT

In many countries, International debt is needed to secure development goals, especially by governments not able to access finance from other sources, or those who are charged high interest rates because of their low sovereign debt rating. Many emerging economies such as those in Africa may not be able to attract direct foreign investment. In order to continue investments in the economy, they can turn to bilateral debt or institutions like the IMF and the World Bank. Trade financing is another option that helps in trade development, a growth strategy of many developing countries.

International trade financing helps exporting countries, especially in reducing trade deficit by spurring exports. Rich exporting countries can facilitate trade finance guarantees to importing countries through export credit agencies.

International debt has advantages not just for governments but for corporations and individuals as well. Corporations can raise international debt in different currencies. The currency differential doesn't just diversify risk, it helps shop for lower interest rates in a limitless international market.

International debt has advantages for individuals as well. Diversify your investment portfolio beyond equities. Invest in international debt through bonds and make substantial profits. There are risks, too. Mitigate those risks by investing in different currency bonds. For instance, a Japanese yen bond could be bought by U.S. citizens and they could hedge dollar risks by investing in yen bonds and earn interest in yen. This way, you could also play off the risks of individual currency depreciation.

Once again, this is an incredibly risky proposition, with factors beyond control of the investor, presenting unacceptable unknowns.

THE PROS & CONS OF BORROWING MONEY FROM THE IMF

The International Monetary Fund (IMF) was founded in 1944 for the sake of facilitating international trade. Its purpose is largely to lend money to struggling governments that cannot pay for necessary imports. It is financed largely by powerful banks attached to its larger members such as Japan, the United States and Germany. The role of the IMF remains intensely controversial.

Economy Watch, a well-known online journal, writes that the IMF serves primarily to reduce global financial risk. The journal points to IMF success in Poland, the Czech Republic and much of Asia. The IMF has helped reform economies and make them into substantial successes. The risk of letting poor countries simply fail is immoral, since this would penalize the poor and middle classes for the sins of its elite financial class. According to Economy Watch, governments are too irresponsible in macroeconomic reform to be trusted with these major decisions. An experienced, outside agency should be entrusted with the task to root out corruption and mismanagement.

Financial writer Carolyn Lochhead, writing in the "San Francisco Chronicle" during the 1997 Asian meltdown, holds that the IMF has empowered mismanagement, not reformed it. She points to major IMF failures in Pakistan, Russia, Indonesia and Thailand as proof of IMF incompetence. What the IMF does, according to Lochhead, is bail out the bankers and firms who have destroyed the economy in the first place. Rather than root out this kind of incompetence, the IMF loans more money to it.

Development economists John Cavanagh, Carol Welch and Simon Retallack wrote in 2001 that the IMF demands structural change, in the form of austerity policies, that creates poverty. If you want to borrow money from the IMF, be prepared to give up national sovereignty and independence.

[Ironic, given that Boris Johnson promised soveriegn independence, but Tory policies are driving the country into the arms of the IMF]

The IMF demands that social spending be cut, wages frozen, the public sector slashed and unions eliminated. The result has been wealth for a tiny elite, and dire poverty for the masses of the population. The IMF cares only about GDP growth and stability, not the good of workers, the poor or the middle class. IMF dictates that come with loans mean the oversight of the economy by the IMF, which means oversight by major bankers. It is a formula for not only poverty, but also a new form of colonialism and domination by the rich.

PROBLEMS IN INTERNATIONAL FINANCE

According to EconomyWatch.com, international finance is a study of economics that deals with "exchange rates and foreign investment and their impact on international trade." In other words, it pertains to the financial affairs of government institutions, their investments and how this impact a currency's value on the international market. In the wake of what seems like a tidal wave of financial crises across the globe, it has become clear that international finance is riddled with complex problems.

One of the key problems facing the world of international finance is the rate at which governments are borrowing or taking out loans to keep the government functioning. Government borrowing impacts the value of its currency. If a government has $10 million dollars in loans, but has a high gross domestic product, its financial health would likely be assessed as good, as it would be able to pay the loan off with ease in a shorter amount of time. This confidence, via complicated financial equations, translates into a higher value for the country's currency.

On the other hand, a country with a large amount of debt that it will not be able to repay in the near future will see its currency's value tank. There are no limitations on government borrowing today, which puts even super powers like the United States at risk of getting in over its head, causing the value of its currency to sink in the global market. When this happens, citizens relying on this currency will have to spend more of it to buy the same things, putting massive amounts of financial strain on a population.

[Which is why we advocate an AgriDollar, against which private citizen will have something tangible to fall back on, when their politicians

default. The ability to trade in grain or other foods suitable

for longer term storage, to stave off stravation from any food

crisis. Or, face cannibalism.]

INTERCONNECTIVITY VS. SOVEREIGNTY

In today's financial climate, the economies of the world are inextricably interconnected. On some fronts, this is perceived as a good thing, as it forces, to a certain extent, a minimal level of diplomatic interaction. However, because the ailment of one economy will inevitably affect the rest, tensions in negotiations over international finance have arisen in regard to global well being and sovereignty.

In the European Union, for example, the collapse of the Greek economy caused countries like France to call for a bailout, while Germany argued that it would not provide financial assistance to another country while trying to keep its own afloat. While Germany eventually agreed to provide financial backing to stabilize the debt crisis in Europe, a conflict of priorities exists between worldwide and national interests, and until a balance can be struck, the fate of every nation's economy could be impacted.

[The UK made enemies of the EU in leaving the Union (common market), who now have no obligation to bail out bozo British politicians. Hence,

Bojo the Clown of

Europe]

Sometimes, the ever-increasing total of international debt and the potential economic insecurity it could unleash is daunting thanks to over $250 trillion owed around the world in 2019. Leading the pack in foreign debt examples is the United States, owing more internationally than any other country and amounting to $67,000 of debt for every American citizen. Policy makers and economists bicker about whether types of external debt matter. Does it, and why does the U.S. owe so much internationally?

US DEBT LEVELS

The amount of national debt, or the deficit, in the U.S. is over $23 trillion, up by over 15% in under three years and is expected to grow by another $6 trillion by 2029 — and that’s just “on the books” debt. Of that, about 30% — nearly $7 trillion — is owed to foreign governments and is money the U.S. borrowed as operating costs, essentially. Over a third of that debt is owed to China and Japan.

Why would foreign governments loan money to the U.S., though? In the case of China and Japan, loaning money to the U.S. to help the government accomplish its tasks and keep the American economy strong keeps the American dollar strong. This sounds counterintuitive, but a higher U.S. dollar means merchants, manufacturers and citizens in the U.S. have buying power, which is good for Chinese and Japanese export business. Hence, helping the U.S. economy stay strong is good for their economies.

[Talk about inverted thinking. Why not have no borrowing, less strain for the private citizen looking to lead a low carbon lifestyle]

There are divided opinions on America’s debt, but they all agree that it's good that America's debt is in its own currency. If that $1 trillion plus owed to China was issued on the yuan, a rising yuan would significantly increase the U.S. debt, but being U.S. dollar debt means the only thing affecting international debt is the interest accumulating.

International debt should not affect small businesses, just like the national deficit doesn’t — in theory. Much of the debt comes from money owed to Americans through Social Security, armed forces payroll and so on. However, there are other prior financial commitments not yet due that economists say could triple the deficit to $70 trillion.

The interesting number in 2019 is the $3 trillion racked up in the past three years because that recent debt increase is from revenue shortfalls after reducing domestic tax rates. The Federal Reserve Chair Powell cautioned that if debt continues to outpace the economy, it will be a problem. If so, the quick solution by the U.S. government would be raising domestic taxes, which would impact all businesses through taxes owed and also through tighter public spending, and incomes may decline under higher taxes.

For small businesses depending on imports from China or Japan, the U.S. debt owed to the Asian nations is advantageous because in a way, holding so much American debt creates a mutually beneficial relationship — but it’s also an insurance policy. If either were to call in their American debts, the American dollar's value would plunge but so would the debt value owed to the two economic powerhouses. Even if China or Japan merely sold their U.S. Treasury holdings to raise capital, it would hurt the American dollar so much that any capital raised would be at a loss. China in particular is happy to maintain the status quo, as it has made its economy the world's strongest thanks to Chinese currency management making its products so attractive to U.S. consumers.

THE MAIN ELEMENTS OF A FINANCIAL CRISIS

An economic downturn caused by a shock in the financial markets may define a financial crisis. This shock is usually the collapse of an economic bubble, which may be found anywhere from the real estate markets and stock markets to the labor markets. Following a bubble's collapse, the main elements and effects of a financial crisis include bank panics, credit crunches and a recession.

The cause of an economic bubble is when the price of a group of assets is much higher than their actual worth. Increase in pricing is a result of an increase in purchases for that given asset. It is known as a "bubble," as it is generally thought that it will "pop" once the markets receive some kind of economic shock. An example of this includes the sub-prime mortgage crisis of 2006 when the price of housing was relatively high with respect to its value. When people defaulted on their mortgages, prices crashed due to the large increase in selling. Other bubbles in history include the dot.com bubble in the 1990s due to the over-investment in dot.com stocks. When these companies began posting losses, their stock crashed.

Negative economic growth generally defines a recession. A financial crisis is one factor that may cause a recession, primarily by means of a fall in investment. A fall in investment may also lead to a fall in employment, as new investments require new employees. Falls in employment lead to a fall in consumer expenditure. This has a negative effect on the economy, as consumer expenditure is usually the largest contributor to economic growth. A fall in consumer expenditure dents company profits, which leads to further unemployment and a fall in stock prices. Although the cause of many recessions is a financial crisis, note that not all financial crises lead to a recession.

THE DANGER OF INFLATION

Expansionary policy carries some risks. When the money supply expands, prices tend to rise and currency loses its value. This happened in a big way during the 1920s in Germany and other European countries. Facing a crushing burden of

World War I debts and reparations due by treaty to Great Britain and France, Germany began printing money to pay its bills. Expansion turned to hyperinflation, as the German currency lost all value and the price of a simple cup of coffee reached millions of German marks. The savings of German citizens were wiped out, and only people holding hard assets such as gold had a hope of financial survival. This traumatic experience still affects the country: Although it has the largest economy in Europe, Germany favors restrictive monetary policy, and its central bank aims to slow the rate of inflation by any means necessary.

MEASURING ECONOMIC STABILITY

Firstly, if there were no international borrowing, all those non-productive workers earning large sums from lending and debts, would cease to be a burden on the ordinary citizen. Also reducing the carbon footprint of the nations who managed their economy so well, they did not need to borrow. This is called a Circular Economy. Oh joy!

We bet that almost every country in the world, wished they were in this condition. A balance of what the country can produce without harming nature, against what its population needed to live comfortably. Again; oh joy!

Economic stability means the economy of a region or country shows no wide fluctuations in key measures of economic performance, such as gross domestic product, unemployment or inflation. Rather, stable economies demonstrate modest growth in GDP and jobs while holding inflation to a minimum. Government economic policies strive for stable economic growth and prices, while economists rely on multiple measures for gauging the amount of stability.

A modern, national economy is too complex to summarize in a single measure, but many economists rely on GDP as a summary of economic activity. Changes in the GDP over time provide a measure of stability. The GDP measures the total output of a nation’s economy in inflation-adjusted monetary terms.

Other measures of economic stability include consumer prices and the national unemployment rate. Government agencies collect monthly and quarterly data on economic activity, enabling policy makers and economists to monitor economic conditions and respond in unstable times.

A modern, national economy is too complex to summarize in a single measure, but many economists rely on GDP as a summary of economic activity. Changes in the GDP over time provide a measure of stability. The GDP measures the total output of a nation’s economy in inflation-adjusted monetary terms.

Other measures of economic stability include consumer prices and the national unemployment rate. Government agencies collect monthly and quarterly data on economic activity, enabling policy makers and economists to monitor economic conditions and respond in unstable times.

WHAT IS THE VALUE OF A CURRENCY ?

Currencies were once assessed by the gold standard, which compared currencies to the U.S. dollar and then to the value of gold. However, this was abandoned after WWI. The current method of assessing currency values is based on the floating currency exchange rate, which is a more efficient way of valuing currency from one country to another, even though currency values fluctuate from day to day.

[We strongly refute any notion that fictitious currencies based on nothing tangible or measurable in terms of sustainable output from planet earth, can be seen as efficient. More, it is not efficient, unless linked to food to feed the population, and energy to keep the wheels turning. One significant issue is corruption in politics and stock markets, leading to billionaires who have not had to lift a finger or raise a sweat, to rape the workers, making them financial slaves for all their lives.]

ECONOMIC TWIN DEFICITS

A twin deficit occurs when a nation's government has both a trade deficit and a budget deficit. A trade deficit, also known as a current account deficit, happens when a nation imports more than it exports, buying more from other countries and foreign companies than it sells to them. A budget deficit occurs when a nation spends more on goods and services than it makes through taxes and other financial gains.

There are many factors that can cause a nation to incur a twin deficit. As with the U.S. in the early 1980s and early 2000s, a twin deficit can come into effect if government tax rates are reduced without corresponding cuts in government spending. When this occurs, a government will have a budget deficit due to the negative difference in government income and spending. This can lead to a twin deficit as a government will then borrow money from other nations, which leads to a trade deficit.

Prior to 1930, America enjoyed budget surpluses most years. However, after 1930 government spending began to outstrip income.

[After that the brakes came off, as paper money was printed in excess of natures ability to supply sustainably. The slippery road to

insolvency of planet earth began.]

IS IT SAFE?

The only truly safe investment against corrupt polticians and international agression, is gold and gemstones, in rapidly transportable, or otherwise protected storage, or other safe haven. Pirates of old knew this, giving rise to treasure maps and buried chests.

THE

TOP TEN RICHEST - 2022

1.

ELON MUSK

2.

BERNARD ARNAULT

3.

GAUTAM ADANI

4.

JEFF BEZOS

5.

BILL GATES

6.

WARREN BUFFET

7.

LARRY ELLISON

8.

LARRY PAGE

9.

MUKESH AMBANI

10.

SERGEY BRIN

https://www.eurodad.org/debt_moratorium

https://bizfluent.com/about-7512012-happens-country-declares-bankruptcy.html

https://www.eurodad.org/debt_moratorium

https://bizfluent.com/about-7512012-happens-country-declares-bankruptcy.html